-

The Euro trims earlier gains as the US Dollar strengthens amid rising risk aversion.

-

Israel’s strike on Iran has overshadowed the effects of softer US inflation data.

-

The EUR/USD pullback remains limited, holding above prior highs.

The EUR/USD pair ended its four-day winning streak on Friday, pulling back from nearly four-month highs above 1.1600 to the lower 1.1500s. The retreat was driven by a wave of risk aversion following Israel’s attack on Iran, which prompted investors to flock to safe-haven assets like the US Dollar (USD).

Geopolitical tensions in the Middle East have intensified after Israel struck Iranian nuclear facilities, killing several senior Revolutionary Guard officers. In response, Iran launched a drone attack and withdrew from nuclear negotiations with the US, raising fears of a broader regional conflict and unsettling global markets.

This risk-off sentiment has bolstered the USD, which had previously been trading at multi-year lows on expectations that the Federal Reserve might cut interest rates in September. Those expectations were supported by Thursday’s US Producer Price Index (PPI) data, which showed softer-than-expected factory gate inflation for May. This followed earlier Consumer Price Index (CPI) data showing a moderate rise, easing concerns over inflationary pressures from tariffs—at least for now.

In the Eurozone, final German CPI figures confirmed inflation remains close to the European Central Bank’s 2% target. Meanwhile, French inflation held steady at a subdued 0.6%, and Spanish inflation was slightly revised higher to 2%.

Eurozone Industrial Production data is due later today, but its market impact may be limited as geopolitical developments continue to dominate investor sentiment.

Daily Market Digest: Geopolitical Tensions Revive the US Dollar

- Heightened geopolitical tensions have breathed new life into the US Dollar, following Israel’s airstrikes on Tehran. This triggered a wave of risk aversion, dragging the Euro 0.7% lower from the multi-year highs reached on Thursday. Despite Friday’s pullback, the common currency remains on track for a solid 1.3% gain over the week. Earlier USD weakness was driven by lackluster US inflation data and uncertainty surrounding the US-China trade agreement.

- Thursday's US Producer Price Index (PPI) figures came in softer than expected, rising just 0.1% month-over-month in May versus the 0.2% consensus. Year-over-year, PPI increased by 2.6%, in line with forecasts. Core PPI also posted a modest 0.1% monthly gain, falling short of the 0.3% expected, while the annual figure landed at 3%, just under the projected 3.1%.

- Meanwhile, US Consumer Price Index (CPI) data earlier this week showed price growth moderating, with May’s headline inflation rising only 0.1% from the previous month and 2.4% year-on-year—both below market expectations. These softer inflation prints have fueled speculation that the Federal Reserve may cut rates in September. The CME FedWatch Tool now places the probability of a 25-basis-point rate cut at 60%, up from 50% just a week earlier. The Fed is currently in a blackout period ahead of its policy meeting next week.

- Across the Atlantic, European Central Bank officials continue to strike a hawkish tone, providing relative support to the Euro. ECB President Christine Lagarde's stance was echoed by Governing Council member Isabel Schnabel, who said the Eurozone’s economic outlook remains "broadly stable," with inflation anchored near the ECB’s 2% target. She added that the market’s view of the ECB nearing the end of its rate-hiking cycle is not accurate.

- Final German CPI data released on Friday reinforced the ECB's position, showing consumer prices rose 0.1% month-over-month and 2.1% annually in May, matching both forecasts and April’s pace.

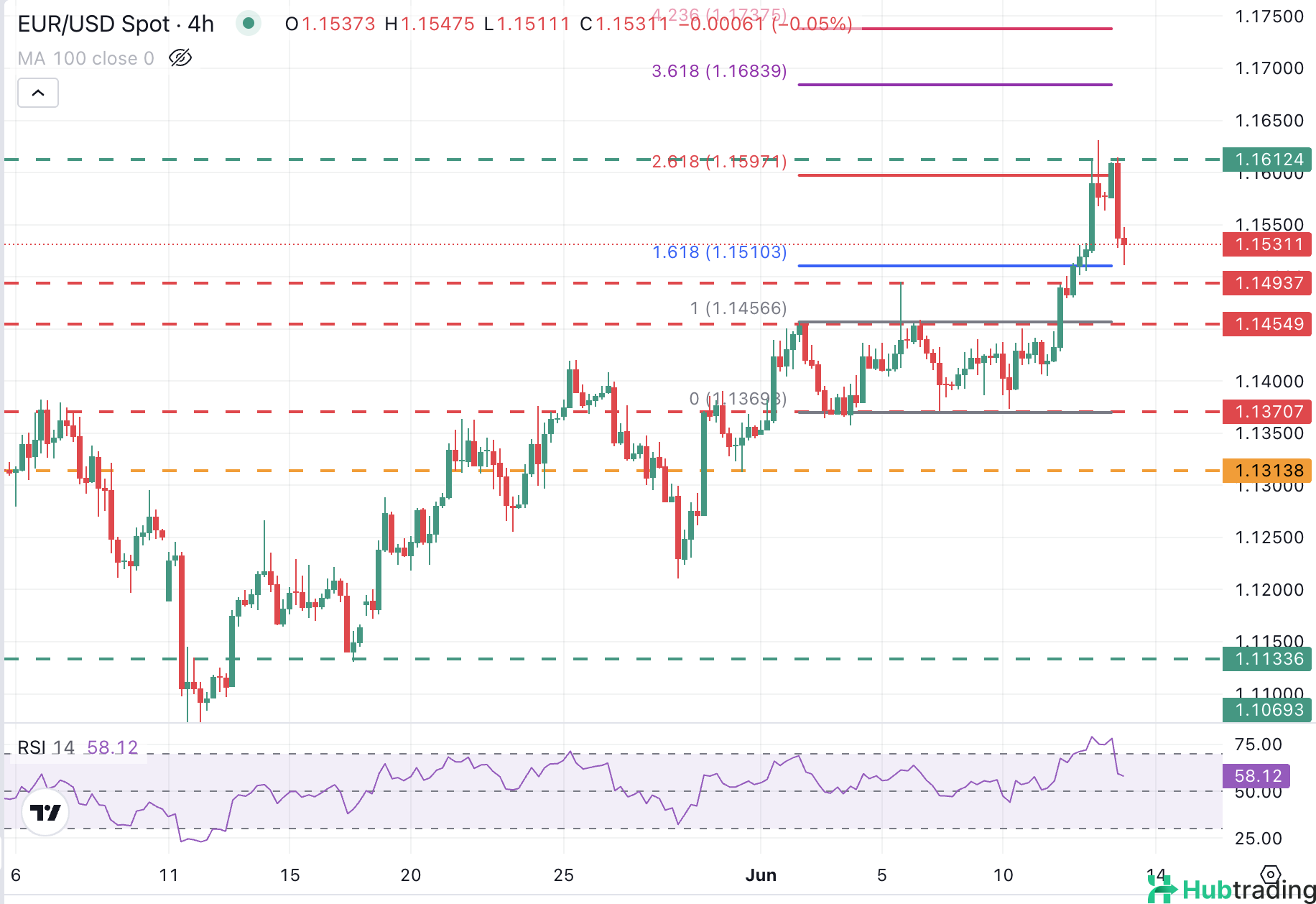

Technical Outlook: EUR/USD Pulls Back, but Trend Remains Intact

EUR/USD faced strong resistance near the 1.1600 level and has entered a short-term correction. However, the broader bullish trend remains intact, with the pair continuing to form higher highs and higher lows. The 4-hour RSI remains above the 50 mark, suggesting underlying bullish momentum still holds.

Immediate support lies in the 1.1495–1.1500 zone, which includes the June 5 high and a key psychological threshold. A drop below this area would expose the next support at 1.1460, aligning with previous highs from June 2 and 10. A deeper break below this level could challenge the prevailing bullish trend.

On the upside, resistance levels are seen at 1.1612 (Thursday’s intraday high), followed by 1.1685, which corresponds to the 361.8% Fibonacci extension from early June’s trading range.

Geopolitical developments will remain the dominant force in the near term, likely overshadowing economic data as traders seek clarity amid rising Middle East tensions.