The Reserve Bank of Australia (RBA) held its cash rate steady at 4.35% during today's meeting, adopting a more dovish tone by removing prior guidance that "it is not ruling anything in or out" and expressing increased confidence in inflation returning to target levels.

The RBA's statement highlighted growing optimism about inflation trends while recognizing ongoing economic challenges. Despite inflation remaining above the 2-3% target range, recent data indicates a more consistent easing of price pressures compared to earlier months.

Key Highlights from the RBA Statement:

- Core Inflation: Eased to 3.5%, though still above the target range.

- Economic Growth: Has slowed significantly, with business conditions at their lowest since 2020.

- Labor Market: Remains tight, with unemployment at 4.1%.

- Policy Guidance: Previous indications on future moves were omitted.

- Economic Imbalances: Supply and demand discrepancies are narrowing.

The RBA emphasized that fourth-quarter inflation data, due in January, will play a pivotal role in shaping policy decisions at the February meeting.

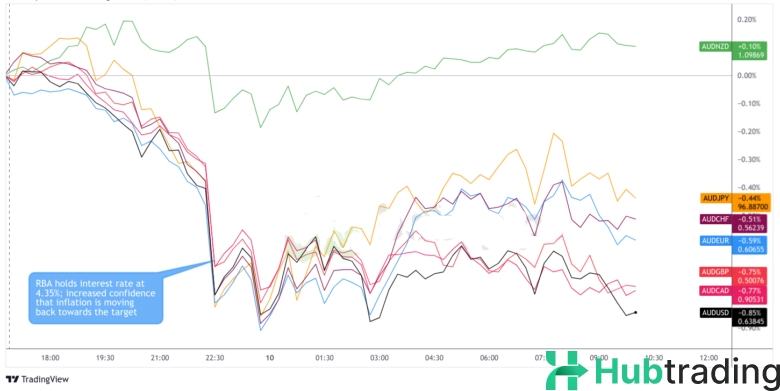

Australian Dollar vs. Major Currencies: 15-Minute Performance

The Australian dollar experienced notable volatility following the RBA’s announcement. Initially, the currency dropped sharply across the board, reflecting market reactions to the RBA’s dovish shift. Losses were most pronounced against the euro, yen, and US dollar.

As the Asian trading session progressed, the Aussie found some support as traders absorbed the nuanced tone of the statement, which acknowledged inflation progress while signaling a cautious outlook on economic conditions. During the London and U.S. sessions, the Australian dollar regained slight ground but remained under pressure, particularly against the USD, CAD, and GBP, staying within a narrow range.

Market pricing has started to reflect the potential for rate cuts as early as February 2025, though this outlook hinges heavily on upcoming inflation and labor market data. The RBA’s dovish tone signals a significant departure from its previous hawkish stance, suggesting the tightening cycle that began in 2022 may be nearing its conclusion.