-

US GDP is projected to grow at an annualized rate of 2.5% in Q2.

-

Markets will interpret the figures through a monetary policy lens.

-

A robust report is needed for the US Dollar to rebound from multi-year lows.

The US Bureau of Economic Analysis (BEA) will release its preliminary estimate for second-quarter Gross Domestic Product (GDP) on Wednesday at 12:30 GMT. Economists expect the report to show an annualized growth of 2.5%, rebounding from the 0.5% contraction recorded in Q1.

A Critical Data Point Ahead of the Fed Decision

The Q2 GDP release is among the most anticipated economic indicators this week and could shape investor sentiment just hours before the Federal Reserve announces its latest monetary policy decision. As the first of three quarterly estimates, this GDP print carries significant market-moving potential.

Following Q1’s surprising contraction, investors are watching closely for signs that the US economy is regaining momentum. Resilient consumer spending, supported by a robust labor market, and easing trade uncertainty have helped calm earlier stagflation fears.

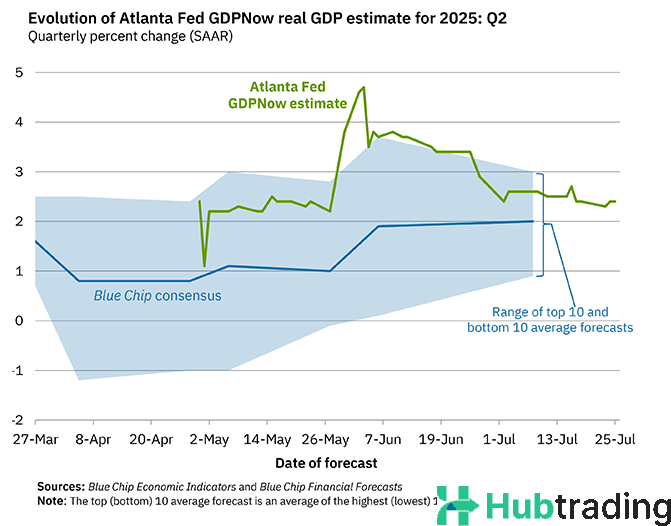

The GDP report will arrive alongside the GDP Price Index (or GDP deflator), which measures broad inflation. This is expected to ease to 2.4% in Q2 from 3.8% previously, indicating a slowdown in price pressures. Meanwhile, the Atlanta Fed’s GDPNow model, a real-time GDP tracker, predicts 2.4% growth as of its July 25 update.

Impact on the US Dollar and Market Sentiment

A strong GDP print could offer the US Dollar (USD) a much-needed lift from recent lows, especially if paired with a hawkish tone from the Fed. The USD is more likely to react positively to stronger-than-expected data than to a mild miss. Robust economic growth, improving consumer activity, and a tight labor market could all support USD recovery.

Still, any immediate reaction may be tempered as traders await the Fed's decision and commentary for further guidance—particularly regarding the possibility of a rate cut in September.

The optimal scenario for USD bulls would be a strong GDP figure coupled with a firm Fed stance, potentially discouraging near-term rate cuts. This could trigger a broader USD rebound, helping the Dollar Index (DXY) recover from multi-month lows.

Technical Outlook for the Dollar Index (DXY)

The broader DXY remains in a bearish trend, having lost about 12% from January’s highs to July’s lows. However, recent price action suggests the potential for a bottoming-out process. A higher low formed in late July, combined with bullish divergence on the RSI and MACD, signals improving momentum.

For confirmation of a trend reversal, bulls need to break above the 99.00 zone, last seen in mid-July. A move past 99.40—the ceiling from June 10 and 23—could open the path toward the psychological 100.00 level.

On the downside, key support lies at the July 24 low of 97.10, which guards the multi-year trough at 96.40. A drop below these levels could drive DXY further down toward the 161% Fibonacci extension of the April-May recovery, around 95.40.